2021 - Franco Angeli

ID: 5101175

Articolo PDF (0,82 Mb)

Consultabile solo con Adobe Acrobat Reader - software gratuito - (scopri come aprire i documenti)

Integrated reporting : much ado about nothing?

119-160 p.

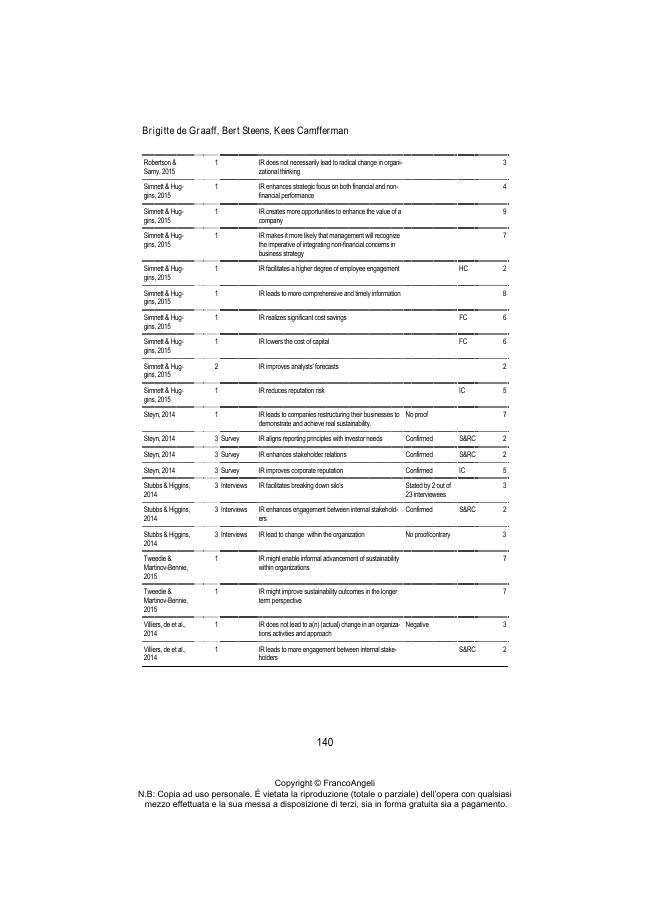

Integrated reporting, which helps companies to share their value creation processes with their stakeholders, has developed rapidly in recent years. Due to the increased attention paid to the International Integrated Reporting Framework issued by the International Integrated Reporting Council, the number of companies worldwide engaging in integrated reporting is continually rising, which is presumably driven by the claimed benefits of this practice. Through recourse to legitimacy theory and management fashion theory, here we provide a preliminary assessment of the development of integrated reporting, alongside considering the potential influence of academic research in its growth. We review the existing body of academic literature on this topic, ultimately identifying 123 claims about the benefits of IR from 29 papers published in 15 journals between May 2011 and September 2016, before proceeding to analyse both the sources and the level of substantiation of these claims.

Our findings suggest that only a few of the purported advantages of integrated reporting are supported by actual empirical evidence, while most of the claims only cite a limited number of primary sources. Based on these results and our assessment of the development of the concept of IR, we propose a future research agenda. [Publisher's text].

-

Articoli dello stesso fascicolo (disponibili singolarmente)

-

Informazioni

Codice DOI: 10.3280/FR2021-002004

ISSN: 2036-6779

MATERIE

PAROLE CHIAVE

- integrated reporting, integrated thinking, management fashion, legitimacy theory, literature review, source analysis

Iva esclusa

PDF

Articolo

Articolo

Leggi le condizioni d'uso