2021 - Franco Angeli

ID: 4986069

Articolo PDF (0,19 Mb)

Consultabile solo con Adobe Acrobat Reader - software gratuito - (scopri come aprire i documenti)

The complexity in measuring M&A performance : is a multi-dimensional approach enough?

89-117 p.

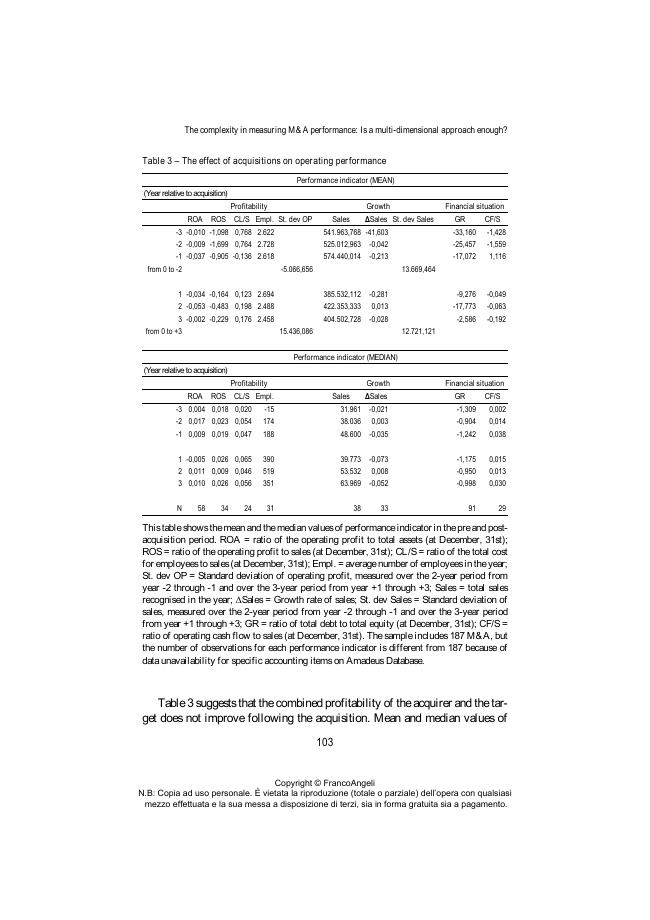

M&A are complex corporate events involving two or more companies and often requiring relevant efforts in order to be successful. For these reasons, both scholars and practitioners are interested in assessing the success rate of M&A and measuring their influence on the corporate performance. Despite the complexity of the M&A phenomenon, previous studies that empirically examine this issue according to an accountingbased perspective, largely adopt single performance measures. Therefore, our study aims to explore whether the use of a multidimensional approach in the development of accountingbased performance measures could provide a comprehensive examination of the change in corporate performance due to complex events, such as M&A.

In particular, this study assesses the performance of M&A concluded in the European context through the development of multiple accountingbased performance indicators that examine: (i) profitability, (ii) growth, and (iii) financial situation. In addition, we analyse a crucial performance dimension, the cost of employment, which has received limited attention from previous empirical research. Consistently with the multifaceted nature of M&A, results indicate that they provide a mixed impact on different performance measures. Therefore, main findings suggest that the measurement of M&A performance should take into consideration different contextual features [Publisher's text].

-

Articoli dello stesso fascicolo (disponibili singolarmente)

-

Informazioni

Codice DOI: 10.3280/FR2021-001004

ISSN: 2036-6779

MATERIE

PAROLE CHIAVE

- M&A complexity, merger and acquisitions, M&A performance, multidimensional approach

Iva esclusa

PDF

Articolo

Articolo

Leggi le condizioni d'uso