2022 - Franco Angeli

ID: 5410554

Article PDF (0,21 Mb)

Pris en charge uniquement par Adobe Acrobat Reader - logiciel gratuit - (découvrez comment ouvrir les documents)

Interdisciplinary research by accounting scholars : an exploratory study

P. 5-34

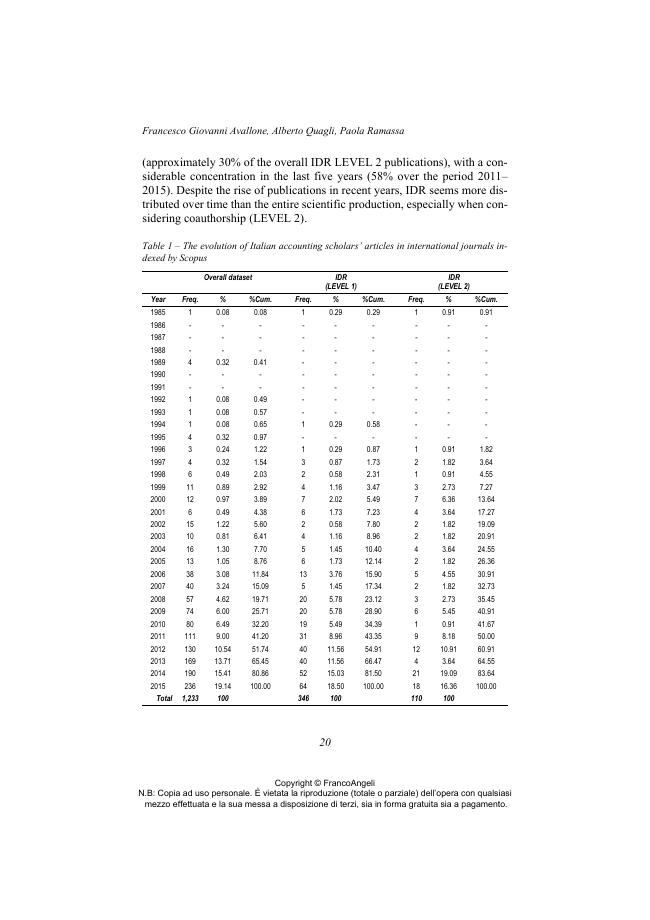

There is a growing consensus around the pivotal role of interdisciplinary research (hereafter IDR) in achieving innovative results and addressing the challenges of modern societies, whose solutions are often beyond the scope of a single discipline. This paper builds on this literature to explore the trends in IDR and its evaluation in research quality assessments in the context of accounting studies by Italian scholars, even in comparison with disciplinary research.

This exploratory study covers a dataset of all articles published by Italian accounting scholars in international journals indexed in Scopus from 1985 to 2015 (1,233 articles). We operationalise IDR as diversity in the subject area of journals where the articles are published and diversity in the disciplinary sector of coauthors. Thus, the novelty of this article is that instead of using a single indicator of IDR, we consider the interaction of two alternative perspectives of analysis. The main findings reveal a relevant increase in disciplinary and interdisciplinary articles, with a comparatively smaller increase for IDR.

Additionally, we observe that IDR by Italian accounting scholars is strongly oriented towards medical publications. Regarding quality evaluation, the findings show a significantly higher evaluation of disciplinary studies compared to IDR according to the criteria followed by the national assessment exercise (VQR). This explorative study contributes to the debate on IDR in two different ways. On the one hand, our study shows a relatively low growth of IDR in the under-researched context of social sciences in a non-Anglo-Saxon setting, where national research evaluations have stimulated radical changes in the features and outlets of scientific production. On the other hand, our results are consistent with the view that papers with a clear disciplinary focus receive comparatively higher evaluations because the standards established for assessment are usually defined within the discipline. [Publisher's text]

-

Articles du même numéro (disponibles individuellement)

-

-

Informations

Code DOI : 10.3280/FR2022-002001

ISSN: 2036-6779

DISCIPLINES

KEYWORDS

- Interdisciplinary research, interdisciplinary research measure, research quality evaluation, Italian accounting scholars

TVA exclue

PDF

Article

Article

Voir les conditions d’utilisation